Emerging Market Investing and Dr Tan Chong Koay

Emerging Market Investing and Dr Tan Chong Koay

Nothingness is infinity

Hello from Exmouth! After a couple days driving and 1,300kms north of Perth, issue #26 is here. Dread it. Run from it. This newsletter arrives all the same. As always, I’m keen to share what I’ve been reading, learning, and compressing. A relevant quote from Tim O’Reilly:

Money is like gasoline while driving across country on a road trip. You never want to run out, but the point of life is not to go on a tour of gas stations.

Here’s the format of today’s email:

Part 1: Emerging Market Investing

Part 2: Under the Spotlight: Dr Tan Chong Koay

Part 3: Bonus Quirky Content - Something to Read, Watch, and Listen

Emerging Market Investing

Similar to my issue on short-selling, hoping to make this a one-stop-shop for emerging market investing. What are emerging markets? I’ll let the CFA Institue explain (from their report further down):

In general, they are not as large, liquid, or transparent as developed markets. The accounting, governance, and legal “rules” by which they operate vary widely, and their return performance is not closely linked with the performance of other markets with which investors may be familiar. To invest in emerging markets, portfolio managers need to accommodate departures from traditional investment practices and frameworks

Harvey Sawikin and Emerging Market Opportunities [Link] [Apple Link]

On common mistakes emerging market fund managers make:

They get arrogant and they forget that they're outsiders. They try to do things that are too funky or get involved in - I saw one asset manager of a portfolio equity fund put almost his whole fund into a private company. He got screwed and wound up losing the fund. I've seen a lot of people just get suckered into very large illiquid things. I learned a lesson myself in 2008 about matching liquidity to the terms of your fund and style drift, I would say, is a big risk in emerging markets because people think that they can do anything. They think, just because they had some good early returns in an emerging market, that they now master that market. They can do private equity there, they can do derivatives, they can do shorting, and become very overconfident. I think that's one of the biggest mistakes.

What enables emerging market growth? [Link]

Michelle Gibley has done a ripper job helping illustrate some proponents of emerging market growth:

Young working-age populations. Working-age people add to economic growth. Retirees do not.

Export strength. Labour costs tend to be lower in emerging markets, driving growth in manufacturing and exports.

Low levels of government debt. Emerging nations tend to produce more than they buy, resulting in trade surpluses. Large state-owned companies involved in exporting are often sources of government revenues, keeping government debt levels low, and funding infrastructure spending or programs to help raise living standards.

Low levels of consumer debt. Debt at the consumer level is also low in many emerging nations.

Growing household income. Rising household incomes means consumers increase their discretionary purchases, resulting in the emergence of a middle-class consumer sector.

Natural resources. Emerging market countries have a disproportional share of natural resource wealth. Countries rich in natural resources tend to benefit as emerging markets industrialize.

Prudent fiscal policies. Many emerging market countries have endured economic crises in the past (almost twice as frequent as Dan R instituting strong fiscal discipline.

Worth noting that the major risks of emerging markets are transparency, competitiveness, and corruption. And yes every market poses challenges in these areas, but the difficulties are magnified in emerging markets.

Investing in Emerging Markets from the CFA Institute [Link]

This 111 page PDF behemoth is a beauty. Legit covers everything: Characteristics of Emerging Markets, Diversification, Return, and Volatility, Efficiency in Emerging Markets, Market Integration and Country versus Sector Factors, Valuation in Emerging Markets. Gives breakdowns of what every emerging market looks like too! I cannot stress how good this one is. I’m a bit of a simpleton and not too fond of reading research papers and the like, but actually enjoyed this one! Download it and save it ASAP!

A couple highlights:

in 1992, emerging countries represented only 9 percent of the world’s equity market cap but their GDP accounted for 19 percent of world GDP. At the end of 2002, emerging markets’ share of the world market cap, as measured by S&P/IFC, had grown to 10.5 percent and their share of world GDP had increased to 20 percent, suggesting that great potential growth in market cap remains

Why is there higher volatility in emerging markets?

• Asset concentration refers to the degree of diversification and concentration that is intrinsic in the indexes for the different countries because the stocks represented in those indexes might not fully represent the actual diversification of the countries’ industry mix.

• Stock market development and economic integration should decrease volatility because of the transition from local to international risk factors and because of the increased diversification of industries within the economy.

• Market microstructure refers to market liquidity and to information asymmetries between traders: As asymmetries decrease and liquidity increases, volatility should decrease.

• Macroeconomic influences and political risk negatively influence the volatility of the stock market, an effect represented by political and macroeconomic risks included in country risk ratings.

Are emerging markets efficient?

Overall, emerging markets do not seem to be efficient. Only about half have a traded long-term fixed-rate instrument in the local currency. All of them have less company-specific information than developed markets. Not surprisingly, only about half of the markets can be considered to exhibit even the weak form of market efficiency.

Manny Stotz and Frontier Markets Investing [Link] [Apple Link]

One of the best. For those that haven’t heard of Manny, he’s the founder of Kingsway Capital, a leading investor in frontier markets and Howard Marks was Stotz’s biggest day one investor. Says all you need to know really. Stotz like emerging markets for their favourable demographics, booming gross domestic product growth, and improving standards of living.

For me, the very best businesses in the abstract are businesses that have the ability to sustain a high return on invested capital without debt. And for reasons we can understand. And they can sustain that with a moat that comes from largely intangible rather than physical assets because physical assets are easier to replicate than intangible assets.

A mismatch in expectations versus fundamentals in emerging markets?

Although we're talking about [in emerging markets] 40% of global population, and 15% global GDP, both fastest-growing again, you're only talking about 50 basis points of global equity market cap. And again, I would bet that those will be much bigger numbers. What has happened basically is that frontiers markets started really to be on investor's radar just before I guess the global financial crisis in the mid, late 2000s. And of course, we had this large crash, which was Western induced financial crisis. That of course also led to a drawdown in these markets. But these markets have never recovered from that, and they have never received a single dollar of QE money, quite the opposite.

Dispelling the Myth of Emerging Markets [57 mins]

10k views on YouTube. Whatta gem. David Bonderman, Binod Chaudhary, and Arif Naqvi discuss the myth of risky emerging markets and how to find return without taking on undue risk. This talk was in 2017, and the following year Arif Naqvi would be accused by investors of misappropriating funds, leading to the provisional liquidation of The Abraaj Group where he worked. Just something to be aware of.

But David makes a great point about how people just seem to lump emerging markets altogether. Go deeper and be more specific!

It's really very idiosyncratic. I mean Nigeria, which is gonna be the world's fourth largest country, is an emerging market. You can argue whether it will ever emerge. On the other hand South Sudan is an emerging market but it's never going anywhere. At least in the timeframe of the humans in this particular ballroom. On the other hand Indonesia is an emerging market, so is Cambodia. Those are great places to invest. So it's all about the particular place and I agree with Eric that this is where a growth is coming, but it isn't coming uniformly. It's coming from some places and not from others and you have to look at the markets individually.

This is my first experience with David Bonderman, and I love it. The dude doesn't give a rats arse. Living his best life.

It just depends on the risks you’re gonna take. You go to the Middle East and you're gonna buy a distillery you've got a different kind of risk if you're buying a distillery in Ireland.

and a little more on risk:

The most important risk of all […] in emerging markets without question is counterparty risk, because this is the single determinant of whether you will make money or not. Who are you partnering with, where are you putting your money, and do you have sufficiently credible partners to help you in your investment journey. So local knowledge is probably the most important element

Dan Rasmussen on the Meb Faber Show [Link] [Apple Link]

As Winston Churchill famously said, “Never let a good crisis go to waste”. And this is a key point of Dan’s research into crises. Investing in crises are where returns are made. And where do crises happen the most? Emerging Markets.

If you think about investing in crises in the U.S., you get a few at-bats or you expand that to developed markets, get a few at-bats. You expand to emerging markets, you’re getting pretty frequently. In fact, I think crises in emerging markets happen about 2X as often as they do in developed countries,

And not just that, when there’s a crisis in the U.S. or developed countries, emerging markets are getting whacked even more!

But he brings up some incredibly interesting points:

I think if you look over the past 30 years, EM has returned like 5% a year with a 22% standard deviation. The S&P 500 has returned 10% [and] 15% standard deviation. So you’ve accepted like wildly more vol[atility] for really mediocre returns, even though emerging markets actually had GDP growth that was roughly 5% a year over that period and developed markets were growing at 2%. So the, sort of, GDP thesis was kind of right but the equity just didn’t translate to equity returns at all.

and the next obvious question is why might that be? Basically, because some emerging markets just get whacked and don’t come back. E.g Japan since the boom and the Philippines.

If you look at 50% drawdown, which again, happen pretty frequently in EM and much more rarely in developed markets, your chances of recovering from a 50% drawdown are like 90% in a developed market, right. You’re investing in France, that French market goes down 50%, you’ve got a 90% chance you’re going to be back up within a year two back up to where you started.

EM drops to about 75%, your chances that you’re going to recover, they’re still good, it’s some good betting odds. But there are a lot of these companies that just go bust and never come back and that’s a risk you’re taking in EM.

And liquidity flows in EM sounds like an absolute mind fuck:

you have these really exaggerated liquidity flows where everyone is really bullish, and then everybody pulls their money out. And that contributes to a lot of problems in these emerging markets. Like, over the long term, foreign investment is good. But the volatility of that foreign investment causes a lot of problems for these countries.

[…]

If you like small value in a crisis, you’re going to really like emerging market in a crisis because the liquidity flows are even more dramatic and even more ignorant

Further Links:

Podcast: Investing in Emerging and Frontier Markets with Kevin Carter, Founder, CIO of EMQQ [Apple Link] [Spotify Link]

Substack: Emerging World. Top 5 stories shaping emerging markets 6 days a week and couple other posts. Pretty neat little Substack!

Substack: Macro Media Lab. About 1x a month Daniel will post a deep dive on a specific emerging topic within India, Southeast Asia, or another developing country

Under the Spotlight: Dr Tan Chong Koay

Each week I provide a little spotlight on an investor or operator I admire. Small feature this week cause I’m on holidays boiiiiiii! Dr Tan Chong Koay is this weeks focus, in a nutshell:

Born in 1950 in Kedah, Malaysia (Northwest Malaysia, bordering Thailand and encompassing the Langkawi archipelago). Dr Tan is one of nine kids!

Got his MBA from Western Illinois University in 1974, before returning to Malaysia as an investment executive in South East Asia Development Corporation. Would later be a fund manager with Arab-Malaysian Merchant Bank, which was then the largest merchant bank in Malaysia.

In 1994 he founded Pheim Asset Management Sdn Bhd, Malaysia and founded Pheim Asset Management (Asia) Pte Ltd Singapore in 1995.

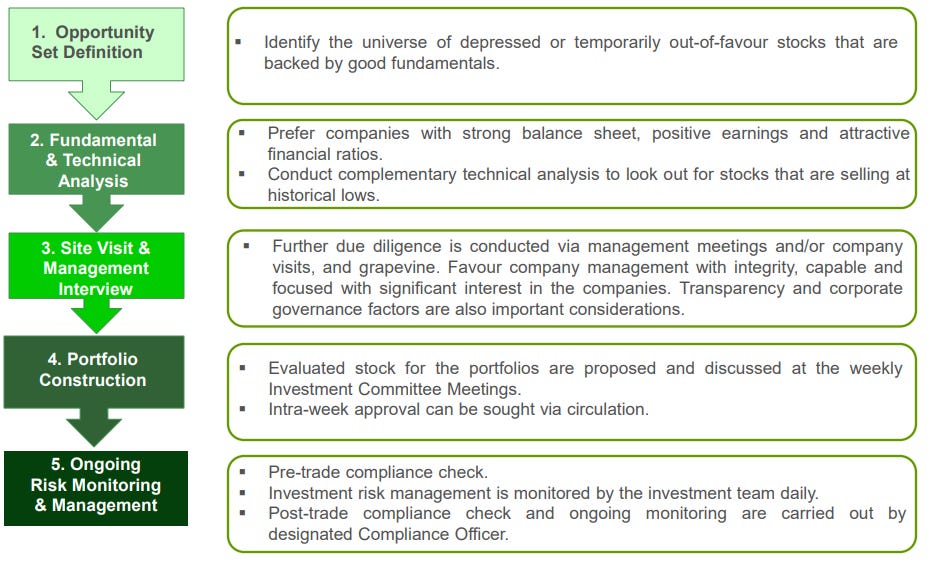

Pheim’s Investment Process?

Most important advice for a young investor?

There is no single factor but in fact there are many attributes that an investor should have to be successful. Having high IQ and doing well in school will help but is never a pre-requisite.

A young investor should learn from successful investors and fund managers about how to identify winning stocks from a business/entrepreneur perspective, and about successful investment strategy and about how to exercise investment discipline. Read widely on current affairs/political/economical events. Next, is to build your experience by investing with real money and going through the cyclical bull and bear run.

Lastly, all the above can only be achieved through research, knowledge and following a proven investment philosophy and criteria.

AMA with Dr Tan Chong Koay (93 mins)

Interview on The Asian Mavericks [Link] [Apple Link]

Investing is an art not a science. There’s no fixed formula that covers all aspects.

Bonus Quirky Content

Something to read: How Consumer Apps Got First Customers [Link]

Some super cool startup stories from companies that are household names today, yet were in struggle town not too long ago.

Evan [Spiegel] was willing to try anything to get users. When he was home in Pacific Palisades, he would go to the shopping mall and hand out flyers advertising Snapchat. “I would walk up to people and say, ‘Hey would you like to send a disappearing picture?’ and they would say, ‘No,’” Evan later recalled.

I admire the confidence, but damn what do you expect random people in the mall to say! But the top seven strategies of acquiring the first 1,000 users were:

Go where your target users are, offline

Go where your target users are, online

Invite friends

Create FOMO in order to drive word-of-mouth

Leverage influencers

Get press (often viral)

Build a community pre-launch

Something to watch: Alan Watts - The Beauty of Nothingness [3 mins]

This gem in the comments is great:

Have you ever noticed that right before you start writing or drawing, every possibility is available to you? That's nothingness. Nothingness is infinity. Every possibility but no concrete existence. And then when you begin writing or drawing what you do is you put a limit on the infinity. You remove most of the possibilities and you're left with something, existence. This universe is exactly the same. It came out of nothingness, infinity, and it limited itself, and that created significance and existence. Beauty.

Something to listen to: Kitchen Confidential Audiobook [Link]

I’ve read Kitchen Confidential already but listening to Tony tell it is so damn good. Tony passed away 3 years ago on June 8th, so pretty timely. Selfishly, if I could write like anyone it’d be a Bourdain x Matt Levine hybrid. Humourous, knowledgeable, and all whilst not taking yourself too seriously. There’s a tonne to learn from Bourdain, yet he packages it in such a way you constantly entertained. Also highly recommend Bourdain’s interview on JRE. I wish Tony were still here.

Rabbit hole/resource to dive into: The Rabbit Hole [Link]

Gotta include this based on name alone. Blas has an unreal amount of book summaries on his site. Like an UNREAL amount. 650+ summaries we’re talking about here. I’m tempted to start something similar myself. But definitely recommend Blas’ site!

Final thought for the week:

Until next week, have a good one!

- Holiday-mode Kalani

You can find previous issues of Curated by Kalani here. I’m on the web at kscarrott.com and on Twitter @scarrottkalani.

Liked this post? Why not sign up.