Losing Your Edge, Predictions, and Howard Marks

Losing Your Edge, Predictions, and Howard Marks

A big construction is always completed late

*in my best Richie Benaud voice* Issue #22. As always, keen to share what I’ve been reading, learning, and compressing. But first, a quick quote from Chris Dixon:

What the smartest people do on the weekends is what everyone else will do during the week in ten years.

Here’s the format of today’s email:

Part 1: Losing Your Edge

Part 2: Predictions

Part 3: Under the Spotlight: Howard Marks

Part 4: Bonus Quirky Content - Something to Read, Watch, and Listen.

Losing Your Edge

Short and sweet section. And honestly more of an open-ended question than definitive findings. But I thought it’d be a fun exercise to ask: How can you lose your investment edge?

In my humble opinion, there are two main ways of losing your investment edge. Externally and internally.

Externally would be due to things out of your control. Basically, more competition. See the below tweet as an example. Another would be the rise of stock screeners. I feel like everything externally basically means more competition. E.g. smarter people and smarter computers. The number of ways you can outperform is smaller today than 100 years ago due to more competition.

Losing your edge internally would be to things you can control. E.g. significantly growing your AUM. The opportunities available to a $50m fund are vastly different to a $1b fund. And those vastly different to a $50b fund. When I spoke about investors who changed (issue #10), a common theme was that they changed alongside their AUM. They realised what works with a small fund, isn’t feasible when running larger sums of money. If you’re a tech-focused investor, losing your edge may be from getting old and obsolete like the tech you invested in.

Again, tried something different with this topic by being more open-ended. Would love to hear any readers thoughts on ways to lose your edge. Or send me through any relevant sources or information. A surprisingly hard topic to google. Thought it would be way easier.

Predictions

If you’re expecting me to make predictions, I’m sorry there’ll be none of that. Showing investors thoughts on predictions and the reasoning behind them.

In Mobs, Messiahs, and Markets: Surviving the Public Spectacle in Finance and Politics, Will Bonner writes:

…you don’t win by predicting the future; you win by getting the odds right. You can be right about the future and still not make any money. At the racetrack, for example, the favorite horse may be the one most likely to win, but since everyone wants to bet on the favorite, how likely is it that betting on the favorite will make you money? The horse to bet on is the one more likely to win than most people expect. That’s the one that gives you the best odds. That’s the bet that pays off over time.

Charlie Munger

The game of investing is one of making better predictions about the future than other people. How are you going to do that? One way is to limit your tries to areas of competence. If you try to predict the future of everything, you attempt too much. [Source]

John Templeton

In all my 55 years on Wall Street, before I retired to do something vastly more important, I was never able to say when the market would go up or down. Nor was I able to find anybody on Earth whose opinion I would value on the subject of when it would go up and down.

My opinion on this quote? Imagine thinking I’m smarter than John Templeton by trying to predict what’ll go up and down when even he couldn’t find someone to do that. Let alone do it himself.

Peter Lynch

I've been fully invested at the start of all the major declines and I will be fully invested in the next one. I am not a market predictor, that's for darn sure.

Because:

Even in good markets we have declines and trying to predict its direction over the near term is an exercise in futility.

Howard Marks

Saved the best for last. Marks is one of the GOATS on this topic. In his memo in Richer, Wiser, Happier [Link], Marks says

Attempts at market timing are a source of risk, not protection against it.

And this from his from the memo You Can't Predict. You Can Prepare:

Most of the time, the consensus forecast extrapolates current observations. Most predictions for growth, inflation and interest rates bear a strong resemblance to the levels prevailing at the time they're made. Thus they're close to right when nothing changes radically, which is the case most of the time, but no prediction can be counted on to foretell the important sea changes. And it's in predicting radical changes that extraordinary profit potential exists. In other words, it's the surprises that have profound market impact (and thus profound profit potential), but there's a good reason why they're called surprises: it's hard to see them coming!

And another banger from Risk Revisited Again [Link]

It seems most people in the prediction business think the future is knowable, and all they have to do is be among the ones who know it. Alternatively, they may understand (consciously or unconsciously) that it’s not knowable but believe they have to act as if it is in order to make a living as an economist or investment manager. On the other hand, I’m solidly convinced the future isn’t knowable. I side with John Kenneth Galbraith who said, “We have two classes of forecasters: Those who don’t know – and those who don’t know they don’t know.”

And here’s the mic drop quote to finish:

Given the near-infinite number of factors that influence developments, the great deal of randomness present, and the weakness of the linkages, it’s my solid belief that future events cannot be predicted with any consistency. In particular, predictions of important divergences from trends and norms can’t be made with anything approaching the accuracy required for them to be helpful.

Thoughts & Summary

Miscellaneous point if you like listening to predictions: Think hard about who is making the prediction, why they are making one, and what they stand to gain. I’m sure some famous investors don’t believe in predictions, yet some will still make them because it’s free media exposure. Media love a hot take prediction. Just my 2 cents.

Going purely on these mentioned opinions, I think it’s a better use of my time studying whether a business might be valuable, rather than doing elaborate predictions on the overall market. It’s a slippery slope though. Because everything in life is a prediction. By crossing the stress I’m predicting a car won’t hit me. By investing in shares I’m making a prediction. But it reminds me of my golf swing. The less moving parts the better. So for investing, the fewer predictions (particularly fragile ones) the better.

But my biggest takeaway: embrace chaos. Dread it. Run from it. Chaos arrives all the same. Imagine how much brainpower and manhours have been wasted trying to predict the future with millimetre accuracy, only to miss by a mile.

Under the Spotlight: Howard Marks

Each week I provide a little spotlight on an investor or operator I admire.

Howard Marks is this weeks focus, in a nutshell:

Born in 1946 and raised in Queens, New York.

Graduated cum laude from Wharton in 1967 with a major in finance and a minor in Japanese Studies.

Started out as an equity research analyst at Citicorp before working up to senior portfolio manager overseeing convertible and high-yield debt.

Founded Oaktree in 1995, focusing on high-yield debt, distressed debt, and private equity. Oaktree now manages over $150b AUM.

I know they may say “never meet your heroes”, but Howard Marks is one of few exceptions for me. I like Buffett and Munger don’t get me wrong, but Marks was someone I related more to. Which is funny because I bet we’re polar opposites.

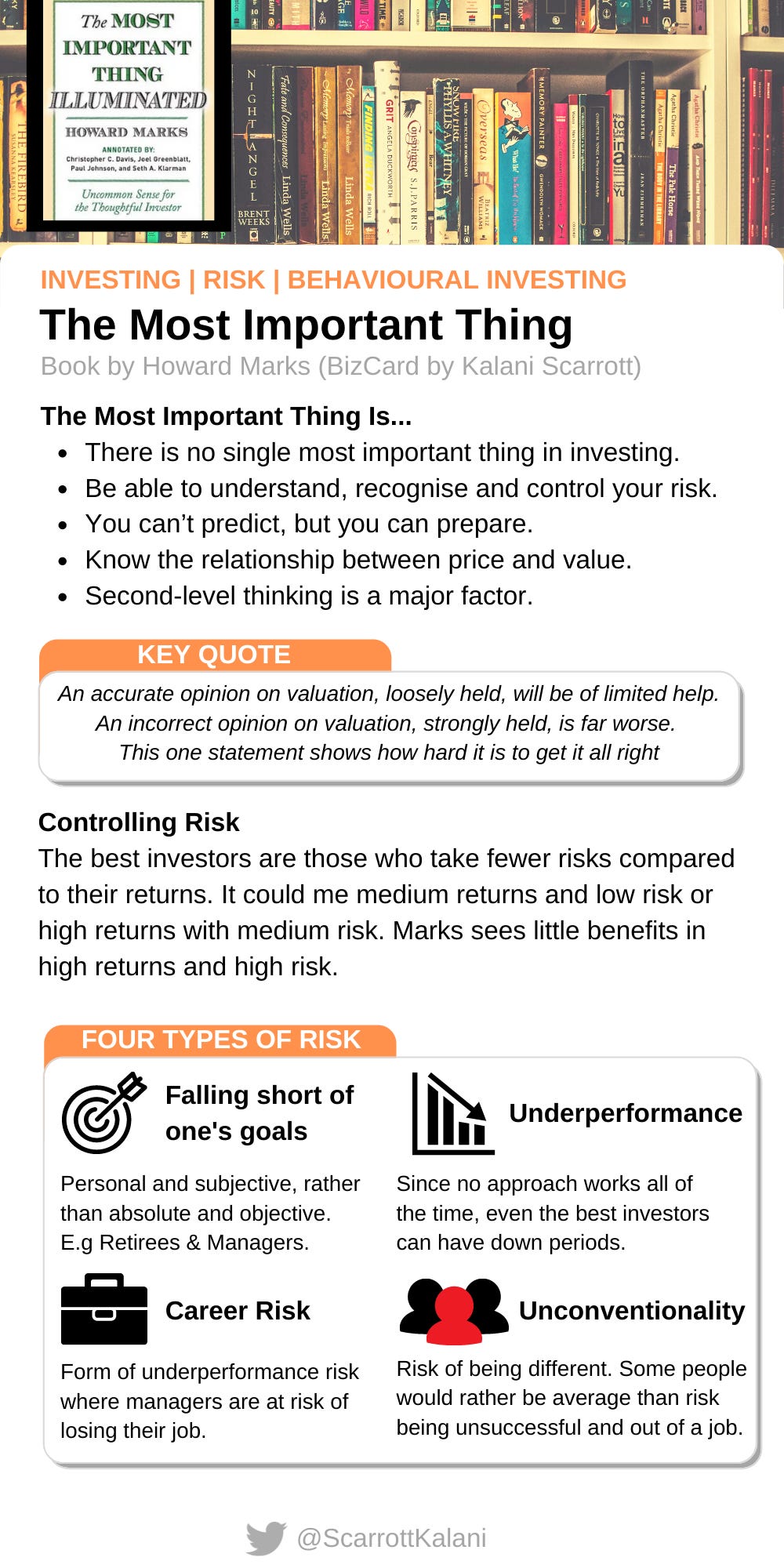

The Most Important Thing [Book Link] [My Summary]

Love Marks’ thoughts on Risk and is honestly one of my favourite books of all time. Particularly for investing. I’d argue it’s been the most influential book on my investment style besides Common Stocks and Uncommon Profits. A couple of my favourite points:

Awareness of the Pendulum

Mood swings of the market resemble a pendulum. At one end would be extreme pessimism, the other extreme optimism. Although the midpoint should be ‘the average’, it spends little time there. Often at either end at overpriced or underpriced.

There are a few things of which we can be sure, and this is one: Extreme market behaviour will reverse. Those who believe that the pendulum will move in one direction forever—or reside at an extreme forever—eventually will lose huge sums. Those who understand the pendulum’s behaviour can benefit enormously.

Recognizing Risk

You can’t control risk if you can’t recognize it. Recognize risk when investors are being too optimistic, being reckless, or paying too high a price for assets. High risk primarily comes with high prices.

a prime element in risk creation is a belief that risk is low, perhaps even gone altogether. That belief drives up prices and leads to the embrace of risky actions despite the lowness of prospective returns.

2020 in Review Memo [Link]

Since the inflation topic is so hot right now, would be rude not to include this:

we’ve had substantial deficits and accommodative monetary policy ever since 2008 and no serious inflation. We’ve seen a 50-year-low in the unemployment rate and yet not the inflation the Phillips Curve would have predicted. And Japan and Europe have been trying for 2% inflation for years without success. Is inflation a threat anytime soon? The answer’s clear: who knows?

Marks on Masters in Business [Apple Link] [Transcript Link]

Marks has been on MiB a few times now and I honestly love every appearance. Some applicable thoughts on the institutional investor versus the individual investor:

Institutions don’t make investments, people make investments for institutions.

And you’re right, those people have emotions too, those people are bombarded with the same news that the mom-and-pop investor is, news is good, news is bad, taxes up taxes down, this company beat, this company fell short, end of the world, you know, trees growing to the sky, whatever it is everybody gets those same inputs, everybody has emotion.

So it’s not true, now the institutional investor may be better educated in finance, may have more experience et cetera, but it’s just not that easy in general. The professional has the advantage of doing the things full-time but guess what the mom-and-pop investor has the advantage that they can’t get fired.

The institutional investor has to worry about getting fired and that makes it hard to do the right thing at the extremes. You know let’s go back Barry to the fourth quarter of ’08, Lehman Brothers has gone bankrupt the stock market is cascading down, bond prices are collapsing, and you had to buy, but maybe you say, you know what, if I buy today and the market goes down further, maybe I will lose my job so I can’t do it.

And the personal concerns make it very hard even for the professional.

Overall this is one of my favourites because if you behave the same as everyone else, you’ll achieve the same as everyone else:

In short, being right may be a necessary condition for investment success, but it won't be sufficient. You must be more right then others... which by definition means your thinking has to be different.

Bonus Quirky Content

Something to read: Does Life End at 35? [Link]

Not a morbid article I swear! More about how producing your best work may come in your later years. Play the long game! This paragraph packed the biggest punch for me:

My grandpa's story made me reflect upon the worship of youthful achievement and our drive to get it all so early in life. I, like many other insecure overachievers, feel an urgency to do big things. Deep down I know this anxiety is root in fear. That I'm not actually any good. That I will waste my shot at life and be a disappointment. So I strive for a quick success because I need to validate my worth. After that I can relax and everything will be plain sailing. Right? Instead, this warped expectation more often leads me to behave in a manner that's unsustainable and counterproductive.

I find it’s easy to get caught up in the short-term scramble. So love a little bit of long-term refocusing every now and again. Because the long term is what I’m aiming for with this newsletter. I’m gunning for #100. And once I reach #100 I want #1000. Which is just under 20 years for those playing along at home. But I’m dead serious. The style may change. The length may change. The ideas may change. But I really enjoy sharing this. Both as an outlet, but also as a branch that has connected me beyond expectations. I’m so grateful to be able to do this. And I’m loving every second.

His advice to me: Don't be in so much of a rush. Be easier on yourself. Comparing yourself to what others are doing is a waste of time. He also adds an old Chinese saying "大器晚成" - A big construction is always completed late.

Something to watch: A Week in the Life: Madelene Sagström [68 mins]

This is the beauty of YouTube. Creators going in-depth where others won’t. For a channel with 76 thousand subscribers, they’re punching well above their weight. Honestly, think this is better than watching a normal golf round. Well shot (pun intended) and edited. Just a decent watch if golf is your thing.

What's the thing that people don't realize about about life out here?

I guess that it's more than just thursday through sunday. […] it's easy when you watch TV, you see the people that are up in the lead and that are shooting good scores. We always stop we always tell people when you're out watching a golf tournament, watch the people that are on the cut line because that's where you see the real grit. L

ike that's when you can see the difference of am I gonna make a paycheck this week why am I not.

Something to listen to: Will Schoeberlein on Think Like an Owner [Link] [Apple Link]

You may know Will on Twitter as @willschoebs, where he posts super useful insights on Japanese businesses and stocks. Really enjoyed this one, one of my recent favourites. Learnt a tonne of new things, gained a new and interesting perspective, and was overall enjoyable. What more can you ask for? Also, I’m 100% here to echo Will’s thoughts on Twitter:

If you’re smart about who you follow and you’re an engaging member of the community, if you will, I found that everyone’s really very nice. There’s tons to learn, tons, tons, tons to learn, and […] There’s no better way to learn more and get better connect with people then start.

[…] I was writing, putting it out there and I’m sure most of it is still ramblings that most people ignore. But at least for myself, it’s been a great way for me to express some of my thoughts to get push back, to get feedback, in the reply section engaging with other very intelligent, successful people, not just on small businesses, learn about stocks and whatever else. It’s just been really great to make, I would call them at least digitally for now, increasingly friends in a lot of way.

Resource / Rabbit hole to dive into: Longriver Library [Link]

Some books and articles on what has taught and inspired Graham Rhodes (@longriver_hk). Biased, but always interested in finding out what influenced fellow investors and operators in Asia-Pacific.

Final thought for the week:

Until next week, have a good one!

- K

You can find previous issues of Curated by Kalani here. I’m on the web at kscarrott.com and on Twitter @scarrottkalani.

Liked this post? Why not sign up.