Position Sizing, Valuation Resources, and Tan Hooi Ling

Position Sizing, Valuation Resources, and Tan Hooi Ling

"I'm not gifted, I'm driven"

Issue #12 coming in hot. As usual, I’m keen to share what I’ve been reading, learning, and compressing. A quick quote from Morgan Housel:

If risk is what happens when you make good decisions but end up with a bad outcome, luck is what happens when you make bad or mediocre decisions but end up with a great outcome.

Here’s the format of today’s email:

Part 1: Position Sizing

Part 2: Valuation Resources

Part 3: Under the Spotlight: Tan Hooi Ling

Part 4: Bonus Quirky Content - Something to Read, Watch, and Listen.

Position Sizing

How much should a position take up in your portfolio? Simple question. Complicated answer.

I wrote last week [Link] on how some of the best investors go about finding their investments. So this week I thought I’d follow up on how they size their investment positions.

Seth Klarman - Max Position Size: 5% of assets (usually)

As part of our risk management, we have never leveraged our portfolios. We do not bet the ranch on any single investment; few positions have exceeded 5% of assets in recent years. We do not generally engage in the short sale of overvalued securities, believing that short-selling could effectively increase, not decrease, portfolio risk in certain kinds of markets.

- Source: Seth Klarman’s letter to Baupost shareholders, December 17, 1999

Bill Ackman - Max Position Size: 5-6% of capital (usually)

We size things based on how much we think we can make versus how much we think we can lose. We’ll probably be willing to lose 5-6% of our capital in any one investment.

- Source: Winter 2015 edition of The Graham & Doddsville Newsletter

and a neat point on his thoughts on diversification

I’ve always had the view that why not own the best ten or eleven investments as opposed to ideas twelve through twenty five, or twelve through one hundred, which is more typical.

I think there are very few great investments at any one time. So the ability to concentrate is an enormously valuable asset of a strategy. The problem with it is it leads to bumpier returns and it leads to more attention on mistakes, or things that aren’t going well. […]

If you want to make high rates return over a long period of time it’s hard to do that being very diversified. I mean if you look through the Forbes 400 wealthiest people in the world most of them made their fortune in one business or a portfolio of two businesses. Very few made it in a portfolio of a hundred.

- Source: Bill Ackman: Why I HATE Diversification? [Video]

Mohnish Pabrai - Max Position Size: 5% of capital (usually)

the old structure was geared towards 10 names with 10% of the fund allocated to each. Now, Mohnish has adopted a 3, 5 or 10 method whereby most positions will be 3 or 5% or the portfolio and if the seven moons line up he will allocate 10% to the investment.

- Source: Pabrai Funds Annual Meeting 2009

Warren Buffett - Max Position Size: 25% of capital (usually)

Saved the GOAT till last. This quote is from when he was running a partnership. Which I think is a lot more relevant compared to now.

We are obviously only going to go to 40% in very rare situations - this rarity, of course, is what makes it necessary that we concentrate so heavily, when we see such an opportunity. We probably have had only five or six situations in the nine-year history of the Partnership where we have exceeded 25%. Any such situations are going to have to promise very significantly superior performance relative to the Dow compared to other opportunities available at the time. They are also going to have to possess such superior qualitative and/or quantitative factors that the chance of serious permanent loss is minimal

- Source: Buffett Partnership Letters, January 20, 1966

What about position sizing for shorts?

Jim Chanos - Max Position Size: 0.5 - 5% of Capital

[Chanos] handles risk with stop loss orders and limiting positions to between 0.5% and 5% (max) of capital. If positions start to get too big, they'll trim them back down to the intended allocation. Also, Chanos revealed that he does not use options or derivatives.

- Source: Jim Chanos On Short Selling: The Power of Negative Thinking

David Einhorn

I was hesitant to use the below quote because I can’t find the original source. But it’s just so damn good I couldn’t leave it out.

We would size the shorts as half as large as we would our longs of the same quality, because when shorts move against us, they become a bigger portion of the portfolio and to give us the ability to endure initial losses and maintain or even increase the investment.

Also, by doing some further digging, his longs would be up to 20% of Greenlight’s portfolio, meaning his short positions would be (at most) 10%. I’d maybe wager even a bit smaller than that.

We decided Greenlight would have a concentrated portfolio with up to 20 percent of capital in a single long idea (so it had better be a one!) and generally would have 30 percent to 60 percent of capital in our five largest longs.

- Source: Fooling Some Of The People All Of The Time

Overall, Fred Liu of Hayden Capital I think makes my favourite point of how to size positions. And if I had to condense this whole section into a single takeaway, it would be this:

there’s no uniform or “right answer” to such an important question. Investors smarter than myself struggle to come to a consensus on it, and I’m starting to believe that the “optimal” method is more dependent upon each investor’s emotional temperament than anything else.

- Source: Hayden Capital Q3 Letter

Valuation Resources

Last-minute addition! Huge resource that was in my bookmarks. Massive credit to Clark Square Capital (@ClarkSquareCap). They post a lot of high-quality material on Twitter, highly recommend giving them a follow.

My good mate Erick Mokaya (@ekmokaya) has compiled all the mentions onto a single page [Link] if you want to bookmark that!

Under the Spotlight: Tan Hooi Ling

Each week I provide a little spotlight on an investor or operator I admire.

Tan Hooi Ling is this weeks focus, in a nutshell:

Born in and raised in a middle-class family in Kuala Lumpur, her father a Civil Engineer, her mother a stockbroker.

Studied engineering in the UK but later decided on a masters in finance and management because “In order to truly make the best decisions and incorporate what the engineering perspective cared about, you needed to be able to talk to the business managers. If you don’t speak their language, you won’t be able to make change.”

Landed a job at McKinsey in Malaysia, who later sponsored her MBA at Harvard – where she met Grab co-founder Anthony Tan. Anthony happens to be the grandson of the founder of Tan Chong Motor.

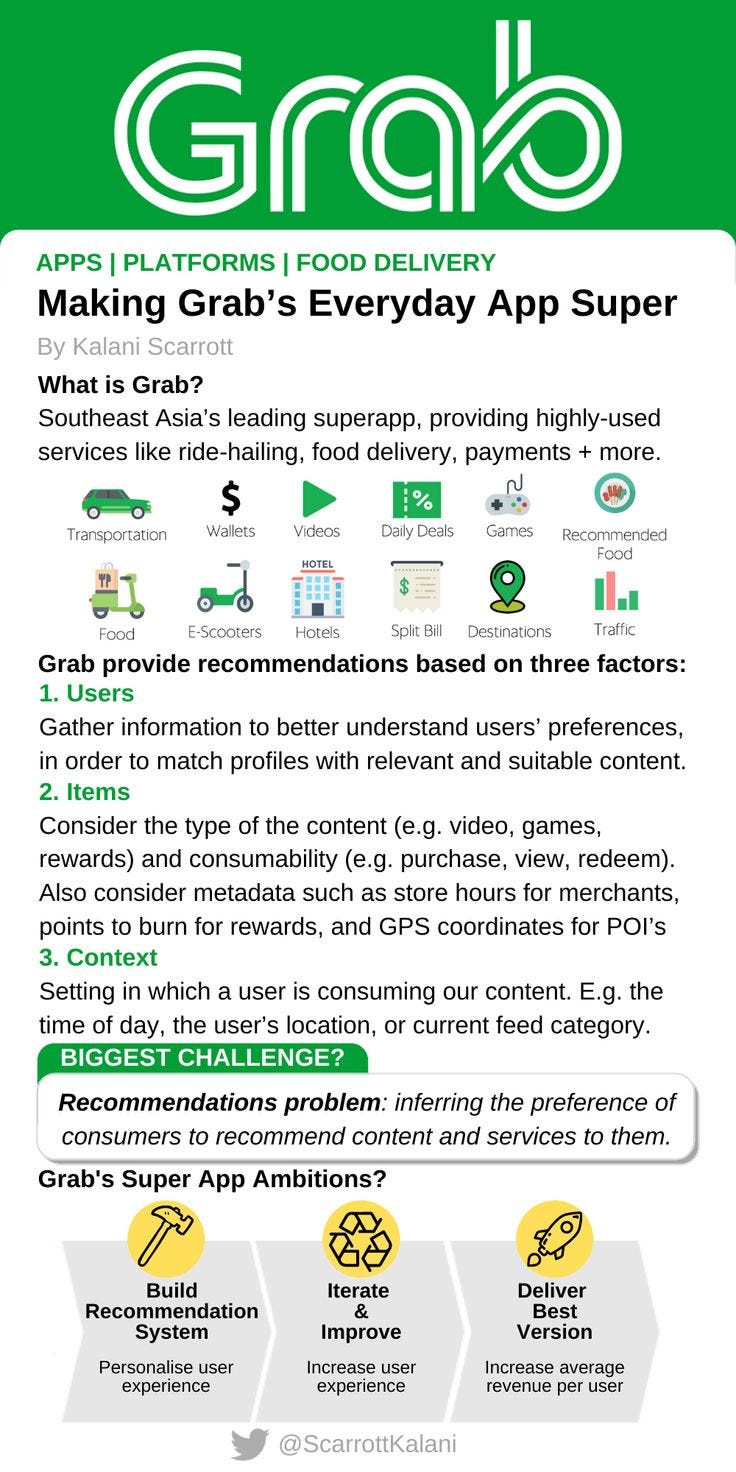

Started Grab as a way to solve Malaysia’s taxi safety problem. Grab is SEA's first-ever decacorn! (10+B valuation)

Hooi Ling Tan’s talk at Goldman Sachs

More about Grab than Tan herself. But shows just how focused Tan is on being able to empower people within the SEA region:

We started with transportation. We started with mobility, but there is so much more right now, whether it’s financial inclusion, whether it’s empowering micro-entrepreneurs and small entrepreneurs, whether it’s just making health care and education better. There is so much more that we can do and that they have seen as consistently [working] hard towards and [taking] action on at speed and skill.

For anyone unfamiliar with Grab, here’s my BizCard:

I’ll finish with this :)

As a woman leading an organisation, you are typically in a minority, so it is never an easy path, but take pride in leaving a legacy that makes it easier for generations of women to come. At the same time, never feel you have to do it all alone. Learn to fail and iterate quickly and find good partners who respect you for you.

Bonus Quirky Content

Something to read: Welcome to the World of Elite Flair [Link]

Bartending competitions. Not someone I knew about in the slightest. But this article gives some nice background to a niche area. You know I’m a sucker for lessons and ideas that are transferable across disciplines. This one is no different:

In a world of copycats, being more original puts you heads and tails above your competitors

Something to watch: David Bowie - Never Play to the Gallery [1 min]

Only a minute long. But pound for pound it’s a bloody good minute.

Always remember that the reason that you initially started working was that there was something inside yourself that you've felt that if you could manifest it in some way, you would understand more about yourself and how you coexist with the rest of society.

and this banger to finish:

If you feel safe in the area that you're working in you're not working in the right area.

Always go a little further into the water than you feel you're capable of being and go a little bit out of your depth.

When you don't feel that your feet are quite touching the bottom you're just about in the right place to do something exciting.

Something to listen to: David Goggins on The Joe Rogan Experience

True story, I ran a marathon on no training after listening to this. Do not recommend. Oprah was about an hour faster than me in case you’re wondering. But seriously, if you can be 10% as mentally tough as Goggins, I think you’ll go places. I don’t think going 100% Goggins is necessarily smart or healthy, there’s certainly lots to learn and takeaway.

What if I’m not good enough?’ We always say that shit and then we try something else. If I’m not good enough, I’m going to fucking make myself good enough; that became my mentality.

You never know until you try! I mean, I thought I’d be pure dogshit at doing a newsletter. But I reckon the below gif is a fair representation.

I'm not the best at anything, I'm not gifted, I'm just driven.

Final thought for the week:

Until next Wednesday, stay hard!

- Kalani

You can find previous issues of Curated by Kalani here. I’m on the web at kscarrott.com and on Twitter @scarrottkalani.

Liked this post? Why not sign up.