Investors Changing, Golf, and Sarah Tavel

Investors Changing, Golf, and Sarah Tavel

"we need to densify the time we have left"

Hey! Issue #10 is here. Different week, same deal, keen to share what I’ve been reading, learning, and compressing. A quick quote from Community:

I mean, if I ever let being bad at something stop me, I wouldn't be here. That thing some men call 'failure,' I call 'living.' 'Breakfast.' And I'm not leaving until I've cleaned out the buffet.

Here’s the format of today’s email:

Part 1: Investors Who Changed Investing Styles

Part 2: Investing and Golf Similarities

Part 3: Under the Spotlight: Sarah Tavel

Part 4: Bonus Quirky Content - Something to Read, Watch, and Listen

Investors who Changed Investing Styles

The Man Who Abandoned Value [Link]

The story is about Arne Alsin, founder of Worm Capital and writer of a column called the “Turnaround Artist” which focused on value-based turnaround situations.

His story basically goes:

Classic value plays won him notice after the tech bubble burst in 2000.

By 2008 his stock picks were struggling — even after the markets bounced back after the crisis.

Eventually, he’s had enough of value investing and:

I just totally gave up and said, “I’m going to do the exact opposite.”

That turnaround did give me a chuckle. I’m not judging him. He can do what he likes, but in terms of nitty-gritty details, how does that actually work? Sell (or short?) all current holdings and go long on companies you’ve shorted or would never normally touch?

Is it really that easy to flip your portfolio and strategy like a switch? Surely you’d have some lingering biases.

I just threw everything out, just literally turned over the table and just, I don’t want to ever see any of this again, I’m going to do it myself — I don’t care how long it takes — from scratch.

Apparently, The Innovator's Dilemma was a key influence on Alsin’s thinking. The book in a [Butchered by Kalani] short summary: outstanding companies can do everything "right" and still lose their market leadership – or even fail – as new, unexpected competitors rise and take over the market. Alsin talks about his realization:

I remember writing about Office Depot, another classic one where their numbers are down. You can buy them cheap, and when they rebound you make a good return. But the problem is, what if they never rebound?

It just hit me like a ton of bricks: Oh, my God, turnarounds are the worst place to be. This is going to be horrible when we replace physical stores with online stores. There’s going to be a hundred turnarounds. And none of them are going to come back because the world’s changed, and that’s going to be true in energy and transportation and on and on and on.

Again, I’m not in a position to judge. His reasoning seems justified and his returns since switching speak for themself. Good on him. Just found the switch interesting.

Has Value Investing Changed? [Link]

In Howard Marks’ latest memo Something of Value, he talks about that maybe, this time it is different.

The value investor of today should dig in with an open mind and a desire to deeply understand things, knowing that in the world we live in, there’s likely more to the story than what appears on the Bloomberg screen. The search for value in low-priced securities that are worth much more should be just one of many importanttools in a toolbox, not a hammer constantly in search of a nail. It doesn’t make sense for value investors to bar investments simply because (a) they involve high-tech companies that are widely considered to have unusually bright futures, (b) their futures are distant and hard to quantify, and (c) their potential causes their securities to be assigned valuations that are high relative to the historic averages. The goal at the end of the day should be to figure out what all kinds of things are worth and buy them when they’re available for a lot less.

At the risk of sounding like a big-brain know-it-all wanker, my definition of value investing has always been as simple as “buy something for less than what it’s worth”. So I’ve never been too hung up on chasing super-low valuation metrics. Do valuations matter? Duh, of course. But it doesn’t need to be trading at 0.3x book value to be interesting. Something can have a P/E of 100, but be tripling revenue YoY and still be cheap. Either way, my opinion is moot. Here’s what Marks thinks:

Value investing doesn’t have to be about low valuation metrics. Value can be found in many forms. The fact that a company grows rapidly, relies on intangibles such as technology for its success and/or has a high p/e ratio shouldn’t mean it can’t be invested in on the basis of intrinsic value

And a nice little historical comparison that may not apply anymore to finish:

The Internet has permeated the world and changed it, and business models have evolved in a way that makes today’s situation incomparable to the Nifty Fifty or the Dot Com Bubble of the late ’90s.

So we’re not in a cycle, but a permanent change has occurred? Don’t ask me. I’m just a lifeguard. Either way, I think this period will be interesting to look back on 20 years from now.

Cigar Butts to Growth

Nearly everyone knows this story, but I’d feel guilty leaving this out. As Warren Buffett and Berkshire Hathaway grew, the available opportunities for cigar butts (beaten-down companies trading well below liquidation value) were less common. Cigar butts didn’t scale and as Berkshire grew, those investments wouldn’t have a meaningful impact on returns. Charlie Munger helped turn Warren from cigar butt detective, to finding incredible businesses at good prices.

Buffett had a buoyant optimism about the long-term economic future of American business, which had enabled him to invest in the market against his father’s and Graham’s advice. Yet his investing style still reflected Graham’s doom-laden habits of looking at businesses based on what they were worth dead, not alive. Munger wanted Buffett to define the margin of safety in other than purely statistical terms.

- Source: The Snowball

which lead to:

Phil Fisher, the apostle of growth, who said that many qualitative factors like the ability to maintain sales growth, good management, and research and development characterized a good investment. These were the qualities that Munger was searching for when he spoke of the great businesses. Fisher’s proof that these factors could be used to assess a stock’s long-term potential was beginning to creep into Buffett’s thinking, and would eventually influence his way of doing business.

- Source: The Snowball

The moral of the story? Even the greatest investor of all time has changed.

Investing and Golf

A fun section that combines two of my passions. Just discussing similarities between the two. Apologies in advance as a lot of this is my own writing.

Risk Vs Reward

Every decision you have to weigh up the risk versus reward of the action. Do you try that big high draw around trees to hit the green? Do you buy that penny biotech stock that could explode (both good or bad)?

There’s no right answer. And the decision is different for everyone.

You have to weigh up what your needs and expectations are, and decide, is the reward worth the risk? For myself, the risk to worry about is blowing it all up. Keep the ball in play. Keep yourself in the game. Keep the initial capital intact.

I don’t wanna wipe myself out by being a hero trying to hit bombs and hoping for the lottery.

Find your Swing, and Trust it

There’s no be-all and end-all way to swing a golf club. Same in investing, there’s no single way to invest and outperform the market.

But in both scenarios, you have to find your style and trust it. You’ll have down slumps. Nothing in life is a constant upward trend of results. But in those downtimes, you’ve got to trust it and analyse where you’re going wrong. Not just abandon ship and say all hope is lost.

When I look back over 17 years at Pershing, the biggest takeaway from the mistakes we’ve made has been that they occurred when we stepped outside of the core strategy that has driven our results over time.

Our core strategy is buying the greatest businesses in the world, super durable, high-quality, simple growth companies.- Bill Ackman [Source]

A key point on the swing. Don’t change it on the course. The range is where you work on it. Same with investing. If you’re a day trader in a position with a tight stop loss, probably not wise to instant pivot to a value investor and buying more as it goes down. I know in the previous section I mentioned investors who changed, even if you asked all those investors mentioned, I’d doubt they’d recommend changing investment styles like you change underwear.

Control What You Can

You can’t control all risks. But you can choose how you approach and react to them. You can’t control the weather. And you can’t control the Fed. You gotta focus on what you can control.

Know your own strengths and weaknesses. And play them to your advantage.

Stay within your circle of competence and control what you can. No point worrying and whinging about matters outside your control. You won’t change anything and it’s a waste of time.

Reset After Every Shot and Pre-Shot Routine

For golf and investing, you really have to play the scenario in your head before it happens. What’s my aim? What could go wrong? If something does go wrong, where might I end up?

Contingencies are helpful in case things do go south. So a little preparation can go a long way.

But when things go south (given enough time they inevitably will), you just gotta roll with the punches, analyse what’s going wrong, and think about your next move.

No point letting previous shit affect future shit.

Long-Term Focus

It takes 17 holes to build a good score, and one hole to ruin it. And as the Oracle of Omaha says, “It takes 20 years to build a reputation and five minutes to ruin it. If you think about that, you’ll do things differently.”

Golf is not a game of perfect. Neither is investing. One bad year or one bad hole isn’t the end of the world. No one is perfect so mistakes happen.

BUT, be wary of the monumental screw-up. It’s easier and more damaging than you realise.

Similarly, if you have a bad start, it doesn’t mean you should pack up and go home. You reset. Focus on the next one.

Play for the long term and don’t fret on the small stuff. But at the same time, avoid blowing up and wiping yourself out. I shared this from Dustin Johnson the other week and applies here too:

I'm the best player in the world, I hit some of the worst shots you've ever seen. But I go find it and hit it again. Obviously not all of them are bad but I do hit bad shots. It's managing those shots and not letting it bother you and going and hitting the next one good.

Play aggressive or play it safe?

My mate on Twitter Sam (@InvestingChef) relating to the recent market run.

We’re seeing a lot more investors go for the green in two as opposed to laying-up, recently.

More like punching a 4-iron from under a tree branch, over the pond to a short-sided pin.

In non-golfing terms, what all these means basically is:

Investors recently seem to be behaving more aggressive than conservative (GME). Sure things can go higher. But you need a lot of things to go right for it to happen than not.

And not only that, the recent form of the market has been crazy good! So why still play so aggresive?

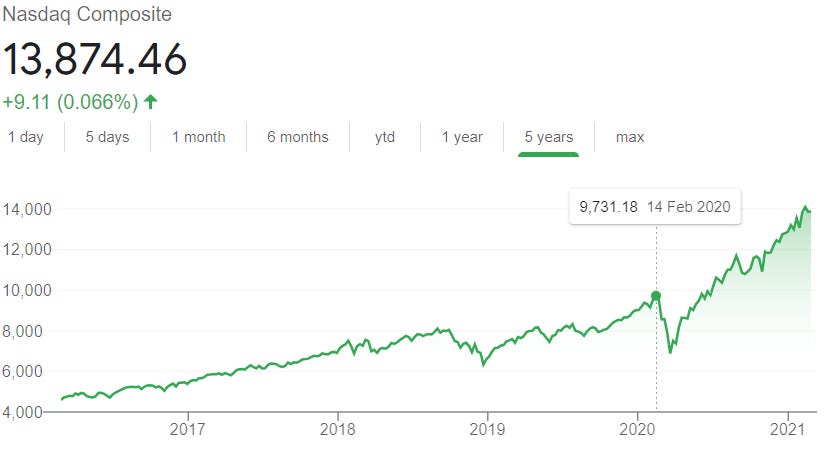

Let me show the numbers perspective:

On the 14th of Feb last year, the NASDAQ was at 9,731. At the time of writing, 13,865.

If you had dumped all your money on Valentine’s day last year, you’d have earnt a nice little 40+ percent return. In a year!

Assuming you’re a genius at invested at 2020’s bottom in March at 6,879 you’d have doubled your money. In under a year!

Sam (and I agree with him) isn’t saying pack it up and go home. But damn maybe stop attacking the green at all costs when you’re comfortably in the lead. In investing lingo, maybe relax on chasing top-tier returns at all costs, accept you’ve had some crazy outperformance, and adjust accordingly.

Let’s assume you’ve actually doubled your money in a year. Do you really give a rats arse if you underperform a little, but sleep soundly at night knowing you’re not balls to walls taking on risk?

Yes, relatively you’ll do worse. But, objectively you’ve doubled your money in a year. Like what more do you want lmao.

Summary

Whether investing or golf, it’s pretty personal. It’s tempting to see others’ success and want to copy it. But often the best use of time is to focus on yourself and just be better than you were yesterday. I’ll finish with this:

I've lost more matches than I care to remember to guys that had a loopy swing, bad address, and a bad grip. Since I merely have a bad grip and a bad swing, I have often found this unfair. More often than not, these guys grooved their bad habits and developed a way to win, often pocketing a car payment in the process.

It doesn't matter where you went to school or how nuanced your thesis may have been, performance ultimately equals smarts in the investment business. Because no style points are awarded in either activity, investing and golf may both be the fairest games of all.

- Jason DeSena Trennert [Source]

Under the Spotlight: Sarah Tavel

Each week I provide a little spotlight on an investor or operator I admire.

Sarah Tavel is this weeks focus, in a nutshell:

Grew up in NYC. Graduated cum laude with a degree in Philosophy from Harvard, where she was also captain of the women's rugby team. (Interesting combo if you ask me!)

One of Pinterest’s first 30 employees. Was the product lead for search, recommendations, machine vision, and pin quality. Would later move into product, becoming Pinterest's founding PM for search and discovery, and launching Pinterest's first search and recommendations features.

Currently works at Benchmark, investing in consumer businesses with a particular focus on marketplaces & social, SaaS, and future of work.

Sarah Tavel - Consumer & Marketplace Investing on ILtB [Link] [Apple Link]

Feels like ILtB has a monopoly on all great business and investing conversations! Either way, well worth the listen.

At benchmark we talk about, we don't really care about how big the initial market is. Because there's actually something really, really right about focusing on something really small from the very beginning. Because that gives you the highest probability of getting to network effects really quickly.

The Hierarchy of Marketplaces [Link]

The marketplace that wins is the marketplace that figures out how to make their buyers and sellers meaningfully happier than any substitute. GMV is irrelevant — a vanity metric that can lead you down the wrong path if you chase it.

See Uber for example:

Kevin Gao’s Compilation [Link]

Another gem from the GOAT. 300 pages covering Sarah’s writing at Bessemer, Pinterest, Greylock, and Benchmark. 14 years of writing! Pretty neato.

At a fast growing startup, your learning cycle is incredibly fast. For example, at Pinterest, particularly early on, if I had a hypothesis I wanted to test, I could ship an experiment fast, and because we already had an incredibly engaged user base, learn from the results within a week or two. Basically, my learning cycle was as fast as you could ask for, which meant I was able to cram an incredible amount of learning into a very short period of time.

On the other hand, I'd often interview product manager candidates who worked at big companies like Microsoft. I'd always be amazed at how little product management they actually got to do over their many years of experience. It'd take them years (literally!) to ship a feature, despite many promotions along the way. It's counter-intuitive, but a brand new startup might actually have a slower learning cycle than a startup that is already a "rocketship". This is because there is a lot of wandering in the desert before you find product market fit.

So if you're thinking of changing jobs, or taking your first, my advice: find a place with a fast learning cycle, and a steep learning curve.

Also, I highly recommend Kevin’s full set of compilations! [Link]

Bonus Quirky Content

Something to read: Phil Jackson: Zen and the Counterculture Coach [Link]

Came across this during last weeks issue [Link] when researching John Buchanan.

Here we have perhaps the antithesis of the authoritarian, shouting control freak, which is unfortunately still the dominant elite coaching stereotype. In the pressure cooker environment of the NBA, and a US social context that tends to over glorify winning and individual achievement, Jackson successfully resists win at all costs influences, takes a moral and spiritual stance, and proves that there is another way to facilitate sporting greatness.

Something to watch: How to Lengthen Your Life [8 mins]

I swear I always have something morbid in the Quirky Content section. Apologies.

We might live to be a thousand years old and still complain that it had all rushed by too fast. We should be aiming to lead lives that feel long because we have managed to imbue them with the right sort of open-hearted appreciation and unsnobbish receptivity, the kind that five-year-olds know naturally how to bring to bear.

We need to pause and look at one another’s faces, study the evening sky, wonder at the eddies and colours of the river and dare to ask the kind of questions that open our souls.

We don’t need to add years; we need to densify the time we have left by ensuring that every day is lived consciously – and we can do this via a manoeuvre as simple as it is momentous: by starting to notice all that we have as yet only seen.

Something to listen to: Ben Crowe - Embrace Your Weird on Dyl & Friends [Apple Link]

Thanks to Mark Laz (@marklaz0) for this recommendation!

our life story is not our life, it's just our story. And we're the author of it. So the good news is we get to write the ending, but the better news is we get to go back to these crucible moments in our teenage years, or 20s, or 30s, where we attached our self worth to an experience good or bad, and we get to go back to those stories, and we get to reframe, or accept or let go or forgive, and we detach ourselves from those experiences.

And through that process, you can reframe and create more positive affirmation based stories that give yourself permission to be imperfect, but also unconditionally worthy.

And that's the opportunity, as we said, we've got to be, you've got to learn to be a good human first and a good athletes second. And if you do that, you can find that unconditional love, which is probably the the panacea for everyone on the planet.

Catchya next week!

- Salami

You can find previous issues of Curated by Kalani here. I’m on the web at kscarrott.com and on Twitter @scarrottkalani.

Liked this post? Why not sign up.