Crisis investing and life outside it

Crisis investing and life outside it

Never let a crisis go to waste

Welcome to the 40 new subscribers of Curated by Kalani! I curate and compress investment topics with a focus on Asia-Pacific, optimizing my emails for maximum return on your time invested. Finding, summarizing and simplifying information so you don’t have to.

Not subbed yet? Join 910 curious legends by subscribing here:

G’day guys, gals and galahs. #35 in ya inbox. Shorter issue this week as I’m in Denmark (the town, not the country FYI), so I’ve been flat out like a lizard drinking. But first, a quote from Morgan Housel to start:

If risk is what happens when you make good decisions but end up with a bad outcome, luck is what happens when you make bad or mediocre decisions but end up with a great outcome.

Here’s the format of today’s email:

Part 1: Crisis Investing

Part 2: Life Outside Investing

Part 3: Bonus Quirky Content - Something to Read, Watch, and Listen

Crisis Investing

How do you react when it all hits the fan? And by “it” I mean shit.

How to Maximize Return During Market Panics by Daniel Rasmussen [Link]

The gold standard of crisis investing. The crème de la crème. The bee’s knees. It’s got everything. Pretty charts. Quantitative stats to back up claims. Covers what works by asset class, what works in stocks and bonds, and has analysis of individual crises. What’s not to love!

The kind of investments that the multifactor model favors are unquestionably not the most popular or well-known stocks. They are often small, with low liquidity, and can be in cyclical or beaten-down industries.

But probably more than anything:

Investors should consider setting aside dedicated capital for precisely these opportunities […] investors cannot plan on keeping their heads when panic strikes. By setting aside capital to take advantage of these opportunities, smart investors are buying insurance for when a rainy day comes. We hope the findings we have illustrated here will give investors confidence and the evidence to act decisively when the opportunity presents itself.

Don’t be afraid of buying on a war scare

In Phil Fisher’s book Common Stocks and Uncommon Profits, Fisher explains from page 143 onwards that investors in a crisis (specifically a war scare), should not be afraid to take advantage. Or maybe more so that it’s the best option you probably have.

What do investors overlook that causes them to dump stocks both on the fear of war and on the arrival of war itself, even though by the end of the war stocks have always gone much higher than lower? They forget that stock prices are quotations expressed in money. Modern war always causes governments to spend far more than they can possibly collect from their taxpayers while the war is being waged. This causes a vast increase in the amount of money, so that each individual unit of money, such as a dollar, becomes worth less than it was before. It takes lots more dollars to buy the same number of shares of stock. This, of course, is the classic form of inflation.

The last bit is the perfect summary. And something I think about a lot. Sometimes stocks and the market might seem poor value. But holding cash or investing in other asset classes you don’t know might be an even poorer value proposition. Damned if you do, damned if you don’t.

The reason for buying stocks on war or fear of war is not that war, in itself, is ever again likely to be profitable to American stockholders. It is just that money becomes even less desirable, so that stock prices, which are expressed in units of money, always go up.

Guide to recessions: When is the next U.S. recession and how should you prepare for it? [Link]

Very pretty presentation. Lot’s of graphics. And a decent quick overview of recessions in the US. On the last slide, there’s a few good nuggets of info:

Recessions have been infrequent. The U.S. has been in an official recession less than 15% of all months since 1950.

Recessions have been relatively short. The current expansion has been longer than the last 10 recessions combined.

Recessions have been less impactful compared with expansions. The average recession leads to a contraction of less than 2% in GDP. Expansions grow the economy by about 24% on average.

An inverted yield curve has preceded each of the last seven recessions by an average of 16 months. It’s one of the most consistent signs that a slowing economy has reached a tipping point.

Equities typically peak seven months before the economic cycle. They also often rebound before a recession officially ends.

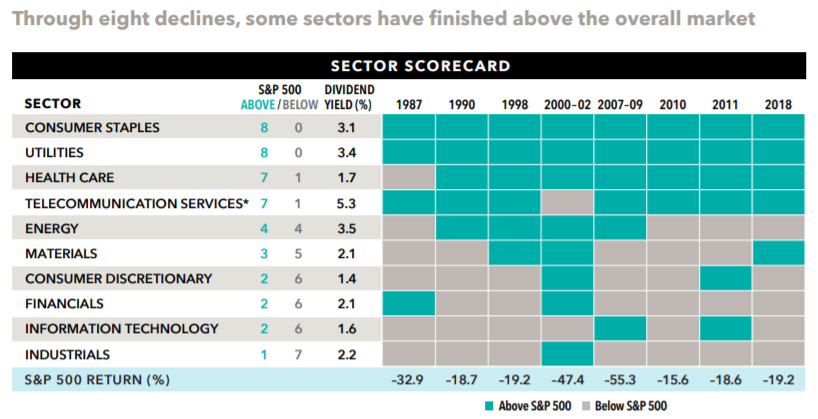

Some equity sectors have held up better during severe declines. Consumer staples and utilities have topped the S&P 500 during each of the last eight major market declines.

And if you can understand this graphic (admittedly it took me longer than it should have), the basic gist of it is Consumer Staples, Utilities, Health Care and Telecom Services have all performed pretty bloody well during declines. But you do you!

Is this permanent?

In John Mihaljevic’s (@JMihaljevic) Manual of Ideas, he mentions how often we see negatives as permanent. But it’s not always so obvious to understand:

One of the crucial judgments regarding a company whose stock price has plummeted due to bad news involves the nature of the crisis—is it temporary or permanent? When fear clouds our judgment—and it does it to all of us—we tend to view the negatives as permanent. Even if they recede over time, we reason, the damage done to the equity will be such that a rebound will fail to materialize. In hindsight, most such misjudgments seem obvious, but they are anything but obvious in the heat of the moment.

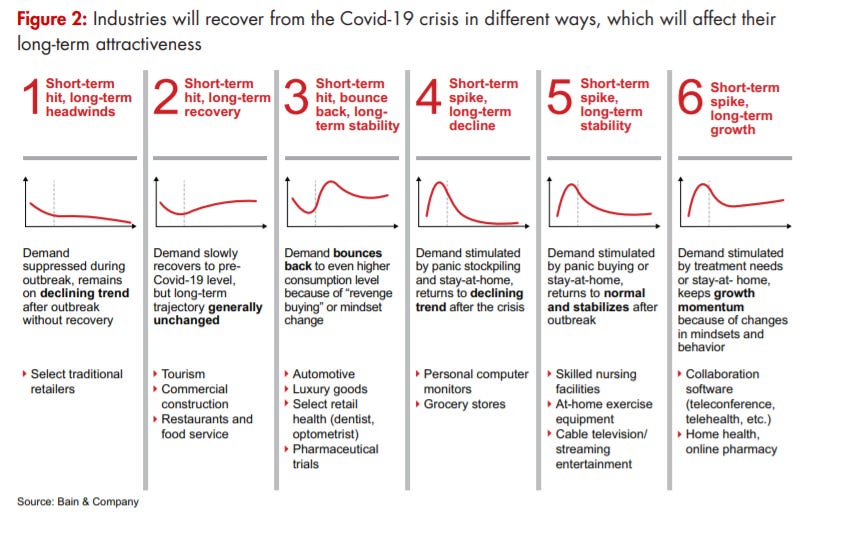

Investing in a Time of Crisis by Bain [Link]

Honestly not an amazing resource, but just wanted to include the below picture to understand the types of shocks and recoveries businesses and sectors may face.

Creating a crisis

More business-related, but Yvon Chouinard (founder of Patagonia), wrote in his book Let My People Go Surfing, that crisis can be a good thing:

Evolution doesn’t happen without stress, and it can happen quickly. Our company has always done its best work whenever we’ve had a crisis. When there is no crisis, the wise leader or CEO will invent one. Not by crying wolf but by challenging the employees with change.

Conclusion

I think this is a neat way to wrap up:

Life Outside Investing

Buffett plays bridge. Bill Ackman loves his tennis. Every other man and his dog in investing seems to enjoy golf. Me included. Does life outside investing affect investing? I think so. I love investing. I basically live and breathe it. But I’ll be dammed if I don’t have a life outside it.

Last week I shared this snippet from Michael Mitchell’s interview: [Link]

"I wouldn’t be a successful investor without good family life. I know others are able to segment their career vs the family and be successful regardless of what happens at home but that’s not me. I know I have a wonderful spouse at home that would support me win lose or draw. That safety net allows me to take bigger swings than I otherwise would."

This comment from Gray Fox on Wall Street Oasis raises a good point:

Investing is a multi-discipline field that requires increasing amounts of qualitative judgment as more responsibility is assumed. Having hobbies, outside interests, and general intellectual curiosity is important. I always ask a similar question now when I interview people. I don't want to spend 50-60 hours/week with somebody that prays to Warren Buffet every night.

Maybe even just for the sake of sanity for your work colleagues, having outside interests is a net benefit.

Duck Decoys [Link]

This one too good to leave out. Paul Tudor Jones has been collecting Duck Decoys since the late ’70s. Before writing this section I had no idea what a duck decoy even was! But they’re essentially a fake duck, painted elaborately and very accurately, to resemble various kinds of waterfowl when hunting real ducks.

But why on earth does he collect duck decoys?

When I hold a decoy in my hand, I want it to be a transforming experience. I try to transport myself back to the last time that a decoy was used in a rig, on a marsh, or in a bay or river, and feel and experience the same wonder, awe, and excitement the last folks that hunted over that decoy experienced. Nothing else really matters after that.

Hey, each to their own! If you enjoy it, more power to you.

Bonus Quirky Content

Something to read: What went right in China? [Part 1] [Part 2] [Part 3] [Part 4]

A deep dive into what changed for China to become the world's largest economy.

Decentralization is important. Deng had the combination of centralized policymaking and local implementation. This allowed him to test different policies in a controlled manner

An effective state is necessary for the transition to capitalism. Unlike Russia where state power had died out, China was able to provide some form of property rights, law enforcement and welfare programs to smoothen the transition.

Bad macroeconomic policy can kill even the best microeconomic policy. The pre-Tiananmen environment had amazing microeconomic policy with the liberalization of the economy, but poor macroeconomic policy with high inflation killed it.

Pradyumna (@PradyuPrasad) is only 17 too! I don’t even want to mention what I was doing at 17. So the big fella putting out high quality work so early is super inspiring.

Something to watch: How Naver Beat Google Search in South Korea [11 mins]

Naver is South Korea’s largest web search engine and also owns the popular messaging app LINE. So this video is a good primer into seeing how this all started. Especially as there’s not too common that a search engine outranks Google!

Also, lmao at companies declining business opportunities under the guise of “oooh it’ll cannibalise our business” only miss out on monster gains and opportunities. Seriously, send me examples of companies that refused to try something out of fear of cannibalisation and it works out well for them.

Cyworld. Founded in 1999, the company signed up over 50% of all internet-connected Koreans by 2003. On Cyworld, users can write blogs, join clubs, and share pictures.[…] They were owned by SK Telecom, one of Korea's dominant telecom companies, and that significantly interfered with their expansion plans. Frankly, SKT had no idea what to do with this special thing they had. They refused to allow Cyworld to expand into messaging, because it would cannibalize their $2 billion texting business. And they did not want to fund a global expansion into Japan like Naver did. […]

Eventually, Facebook broke Cyworld down.

Something to listen to: Ming Maa of Grab – Growing a Super App in Southeast Asia [Transcript Link] [Apple Link]

Originally from Oct 2019 but is a great insight into Super Apps and how Grab approaches expansion.

There’s always room for improvement, but it seems like, based on our experience, in order to win and to do well in a super competitive market, unfortunately, only the stronger survive. And this is all about how fast you learn. Nobody comes into the situation having all the answers. How you can make mistakes quickly and not have any mistakes hurt you fundamentally and grow from that, and be able to learn to fly and execute, it’s not an easy task. That’s why there are not many super apps that are successful and can get to the Decacorn kind of stage.

Something to listen to (from me): Aaron Pek on Compounding Curiosity [Transcript Link] [Apple Link]

Loved this one. And selfishly is a perfect example of why I love doing the podcast. Aaron has become a dear friend and I’m immensely grateful. Just a great down to earth bloke. Plus his knowledge of Malaysian equities is second to none!

My personal recommendation to all foreign investors is to look at small to mid-cap space in Malaysia. There are tons, literally tons of businesses in the small and mid-cap space in Malaysia which are really well run right, and exemplify the same level of stewardship, as compared to the U.S. Companies, obviously by virtue of Malaysia being an emerging market. You will get bad apples here and there, but you also get good pears, or good oranges. I’m not saying that the entire Malaysian small market cap space is filled with these good examples, but there are certainly enough of them.

Bonus investing links that don’t fit anywhere else:

Want to find the next Epic Games? You should be looking at India.

"A few years ago, India's e-sports industry was fiercely underdeveloped. It held just 25 developers, a few million viewers, and was roughly worth $200M USD as a whole. Today there are over 400 game developers in the country, 27M viewers (expected to hit 85M by 2025), and its valued at almost $1B USD."Esports in India PDF by EY

"Esports industry in India would generate an economic impact of INR100 billion between FY2021 and FY2025. […] By FY2025, India will have 1.5 million esports players"Vietnam emerges as Southeast Asia's next fintech battleground

"Many Vietnamese download multiple wallets, pulling up whichever has the best discount for the store where they are shopping. The challenge is getting users to continue using an app without lavish promotions. Is that possible? Pham thinks not. He asked his 40 students in one fintech class if they would keep using e-wallets without discounts. All said no."

Final thought for the week:

Until next week, have a good one!

- South West Scarrott

You can find previous issues of Curated by Kalani here. I’m also interviewing legends at Compounding Curiosity, and learning on Twitter @scarrottkalani.

FYI: You can always hit ‘Reply’ to this email and it’ll be sent to me! Always keen to hear from readers :) Have feedback? Fill out anonymously here.

If you enjoyed this labour of love, consider giving it a “❤️” on Substack or share it with friends using the button below!